CMA Inter Suggested Answers | Dec 24 Law & Ethics | ICMAI Suggested Answers

Table of contents

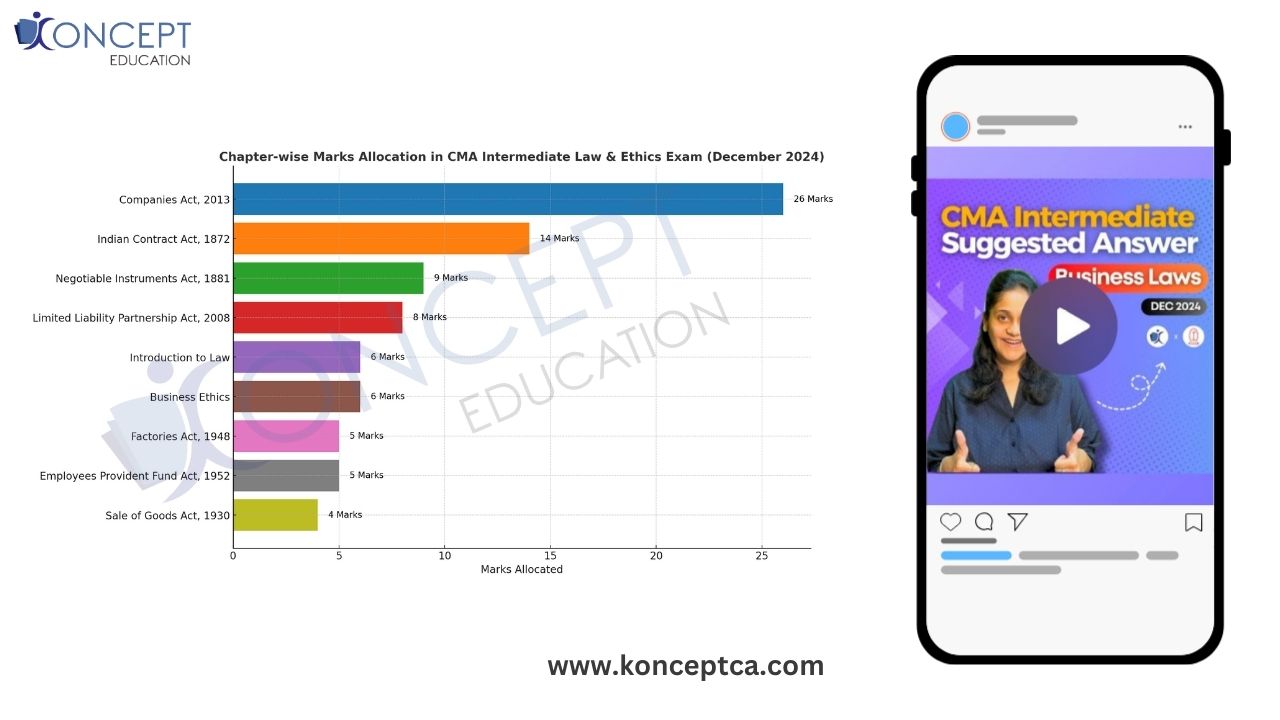

CMA Inter Dec 24 Suggested Answer Other Subjects Blogs :

MCQs

(i) The term 'Alternative Disputes Resolution' takes in its fold, various modes of settlement including ,________ , Arbitration , Conciliation and mediation.

Answer :

(C) Lok Adalats

The term “Alternative Disputes Resolution” takes in its fold, various modes of settlement including, Lok Adalats, arbitration conciliation and Mediation.

(Study Material Page 18 | This Question is also a part of konceptca.com question bank)

(ii) Under which of the following cases, a contract may not be discharged by operation of law?

Answer :

(C) Waiver

A contract may be discharged by operation of law in the following cases

1) Death: In contracts involving personal skill or ability, death terminates the contracts. 2) Insolvency: The insolvency of the promisor discharges the contract. 3) Unauthorized material alteration: Material alteration in the terms of the contract without the consent of the other party discharges the contract. 4) Merger: When inferior rights of a person under a contract merge with superior rights under a new contract, the contract with inferior rights will come to an end.

(Study Material Page 59 | This Question is also a part of konceptca.com question bank)

(iii) In order to push up the sales generally there is a practice of sending goods to the customer with the clear cut understanding that he has option to approve or return the goods within a given period. This type of sales is known as__________.

Answer :

(D) Approval or Sale or Return

In order to push up the sales generally there is a practice of sending goods to the customer with the clear cut understanding that he has option to approve or return the goods within a given period. This type of sales is known as “approval or sale or return”. In such cases, the transaction does not culminate into sale until the goods are approved by the customer and the property in goods still remains with the seller.

(Study Material Page 100 | This Question is also a part of konceptca.com question bank)

(iv) In case the back of a negotiable instrument is full of indorsements, a slip of paper may be attached to the instrument for signing indorsements. Such a slip is legally known as

Answer :

(A) Allonge

An allonge is a sheet of paper that is attached to a negotiable instrument, such as a bill of exchange. Its purpose is to provide space for additional endorsements when there is no longer sufficient space on the original instrument.

(We could not find this question in the ICMAI Study Material)

(v) An individual shall give his consent to become a designated partner in__________

Answer :

(B) Form – 9

An individual shall give his consent to become a designated partner in Form – 9

(Study Material Page 192 | This Question is also a part of konceptca.com question bank)

(vi) According to Section shall 67 be of required the Factories or allowed Act, to 1948, a child who has completed his________shall be required or allowed to work in any factory.

Answer :

(B) 14th year

Section 67 provides that no child who has not completed his 14th year shall be required or allowed to work in any factory.

(Study Material Page 252)

(vii) Withdrawal from the provident fund is not allowed for

Answer :

(B) Marriages of children as Withdrawal from the fund is allowed for the following purposes

(Study Material Page 281 | This Question is also a part of konceptca.com question bank)

(viii) Which one of the following is not correct in regard to share certificate ?

Answer :

(A) The Company Secretary shall issue the share certificate

(Study Material Page 456 | This Question is also a part of konceptca.com question bank)

(ix) The One Person Company (OPC) gives the individual entrepreneurs all the benefits of ___________

Answer :

(D) A company

The concept of One Person Company is quite revolutionary. It gives the individual entrepreneurs all the benefits of a company, which means they will get credit, bank loans, and access to market, limited liability, and legal protection available to companies.

(Study Material Page 345 | This Question is also a part of konceptca.com question bank)

(x) A poll demanded on any question shall be taken withinfrom the time when the demand was made.

Answer :

(D) 48 hours

A poll demanded on any other question shall be taken at such time, not being later than 48 hours from the time when the demand was made, as the Chairman of the meeting may direct.

(Study Material Page 457 | This Question is also a part of konceptca.com question bank)

(xi) Under Section 2(51) of the Companies Act, 2013, who is not defined as a part of Key Managerial Personnel?

Answer :

Section 2(51) of the Companies Act, 2013, key managerial personnel, in relation to a company has been defined as:

iii) the whole-time director;

(Study Material Page 455 | This Question is also a part of konceptca.com question bank)

(xii) If any inspection is refused or if any copy required is not furnished within the specified time, the company shall be liable to a penalty of __________.

Answer :

(B) ₹ 25,000

If any inspection is refused or if any copy required is not furnished within the specified time, the company shall be liable to a penalty of ₹ 25,000

(Study Material Page 436 | This Question is also a part of konceptca.com question bank)

(xiii) Which one of the following is not the criterion for the appointment of an independent director?

Answer :

(B) He shall relate to the promoters of the company.

(Study Material Page 458 | This Question is also a part of konceptca.com question bank)

(xiv) Almost every company now has a business ethics program, mostly because technology and digital communication have made it easier to identify and publicize __________.

Answer :

(B) Ethical missteps

Almost every company now has a business ethics program, mostly because technology and digital communication have made it easier to identify and publicize ethical missteps.

(Study Material Page 473 | This Question is also a part of konceptca.com question bank)

(xv) A proper foundation of ethics requires a standard of __________ to which all goals and actions can be compared to.

Answer :

(A) Value

A proper foundation of ethics requires a standard of value to which all goals and actions can be compared to.

(Study Material Page 474 | This Question is also a part of konceptca.com question bank)

Question 2 (A)

What are different ingredients of the E-contracts?

Answer :

E-contracts are paperless contracts and are in electronic form. It is the change of technology and legal requirements lead to the contract to be in electronic form. E-contract is a contract modelled, specified, executed and deployed by a software system. They are conceptually very similar to traditional commercial contracts. E-contract also requires the basic elements of a contract.

The following are ingredients of the E-contracts-

The main features of this type of E- contract is speed, accuracy and reliability. The parties to the contract have to obtain digital signature from the competent authority and they have to affix the digital signature instead of manual signing. TheInformation Technology Act, 2000 regulates such E-contracts.

In this type of contract, the web site of the offeror acts as a display to the world at large. E-mails are used to negotiate and agree on contract terms and to send and agree to the final contract. An email contract is enforceable if the requirements of the contract are fulfilled. Electronically signed contracts cannot be denied because they are in electronic form and delivered electronically.

(Study Material Page 44 | This Question is also a part of konceptca.com question bank)

Question 2 (B)

Discuss the circumstances under which the liability of the surety is considered to discharged and the liability of the surety is not considered to be discharged.

Answer :

The liability of the surety is discharged under the following circumstances

However, in the following circumstances the liability of the surety is not considered to be discharged

(Study Material Page 73 | This Question is also a part of konceptca.com question bank)

Question 3 (A)

Demonstrate the procedure of appointment of auditor as per the Limited Liability Partnership Act, 2008.

Answer :

Appointment of auditor

A Chartered Accountant in practice is qualified for appointment as an auditor. The auditor(s) shall be appointed for each financial year of the LLP for auditing its accounts. The designated partners may appoint an auditor(s)

If the designated partners have failed to appoint auditor(s), the partners may appoint an auditor or auditors. An auditor appointed shall hold office in accordance with the terms of his or their appointment and shall continue to hold such office till the period

Rule 24 (14) provides that where no auditor has been appointed, any auditor in office shall be deemed to be re-appointed unless

A notice may be in hard copy or electronic form and must be authenticated by the person or persons giving it

(Study Material Page 201 | This Question is also a part of konceptca.com question bank)

Question 3 (B)

Discuss the various types of instruments mentioned in the Negotiable Instruments Act, 1881.

Answer :

There are various types of instruments mentioned in this Act as follows:

(Study Material Page 127 | This Question is also a part of konceptca.com question bank)

Question 4 (A)

Demonstrate claims made under The Code on Wages, 2019 and procedure thereof.

Answer :

Section 45 deals with claims under Code and procedure thereof.

(Study Material Page 326 | This Question is also a part of konceptca.com question bank)

Question 4 (B)

Describe the regulations relating to the payment of gratuity and explain how the gratuity amount is calculated.

Answer :

Eligibility for Gratuity (Section 4(1)):

Rate of Gratuity (Section 4(2)):

Amount of gratuity payable

Gratuity is calculated on the basis of the continuous service rendered by the employee, for every completed year of service or part in excess of six months at the rate of fifteen days wages last drawn. The maximum amount of gratuity allowed under the Act is ₹ 20 lakhs with effect from 29.03.2018.

Formula for calculation of gratuity = Last wage drawn × 15/26 × completed years of service In calculation of gratuity one month is taken as 26 days.

(Study Material Page 263 | This Question is also a part of konceptca.com question bank)

Question 5 (A)

Analyse the relevance and the circumstances for 'Lifting of the Corporate Veil' under the Companies Act, 2013.

Answer :

The separate personality of a company is a statutory privilege and it must be used for legitimate business purposes only. Where a fraudulent and dishonest use is made of the legal entity, the individuals concerned will not be allowed to take shelter behind the corporate personality. The Court will break through the corporate shell and apply the principle/doctrine of what is called as “lifting of or piercing the corporate veil”. The Court will look behind the corporate entity and take action as though no entity separates from the members existed and make the members or the controlling persons liable for debts and obligations of the company.

In the following circumstances, different courts found it necessary to lift the corporate veil and punish the actual persons who did wrong or unlawful acts under the name of the company.

(Study Material Page 341 | This Question is also a part of konceptca.com question bank)

Question 5 (B)

Examine various aspects relating to Directors' remuneration as per the Companies Act, 2013.

Answer :

Remuneration of Directors

(Study Material Page 443 | This Question is also a part of konceptca.com question bank)

Question 6 (A)

Outline the provisions relating to Board's report as per the Companies Act, 2013.

Answer :

Provisions Relating to Board’s Report (Section 134, Companies Act, 2013)

(Study Material Page 446 | This Question is also a part of konceptca.com question bank)

Question 6 (B)

Examine Cancellation or Surrender or Deactivation of DIN.

Answer :

Question 7 (A)

Interpret the relationship between ethics and law.

Answer :

Question 7 (B)

Describe the different kinds of business ethics.

Answer :

Question 8 (A)

Mr. X drew a cheque payable to Mr. Y on order. Mr. Y lost the cheque and was not aware of the loss of the cheque. The person who found the cheque forged the signature of Mr. Y and endorsed it to Mr. Z as the consideration for goods bought by him from Mr. Z. Mr. Z encashed the cheque, on the very same day from the drawee bank. Mr. Y intimated the drawee bank about the theft of the cheque after three days. Review the liability of the drawee bank.

Answer :

Question 8 (B)

Mr. A is a director of PQR Ltd., appointed by its shareholders by passing an ordinary resolution. Only after six months of his appointment, a news was published in a local daily mentioning his name. As per the news, Mr. A asked for a bribe of a huge amount from a supplier of the company. Following this, a month later, shareholders of the company removed Mr. A from the office of the director and appointed Mr. B in his place for the time being at the said meeting.

Now, Mr. A is arguing that his removal before completion of his tenure on the basis of media reports is not only unfortunate but also illegal as the allegation has not yet been proved.

Present your view on the removal of Mr. A and also state whether the temporary appointment of Mr. B is valid or not.

Answer :

Business Laws and Ethics detailed analysis

Ruchika Ma'am has been a meritorious student throughout her student life. She is one of those who did not study from exam point of view or out of fear but because of the fact that she JUST LOVED STUDYING. When she says - love what you study, it has a deeper meaning.

She believes - "When you study, you get wise, you obtain knowledge. A knowledge that helps you in real life, in solving problems, finding opportunities. Implement what you study". She has a huge affinity for the Law Subject in particular and always encourages student to - "STUDY FROM THE BARE ACT, MAKE YOUR OWN INTERPRETATIONS". A rare practice that you will find in her video lectures as well.

She specializes in theory subjects - Law and Auditing.

Yash Sir (As students call him fondly) is not a teacher per se. He is a story teller who specializes in simplifying things, connecting the dots and building a story behind everything he teaches. A firm believer of Real Teaching, according to him - "Real Teaching is not teaching standard methods but giving the power to students to develop his own methods".

He cleared his CA Finals in May 2011 and has been into teaching since. He started teaching CA, CS, 11th, 12th, B.Com, M.Com students in an offline mode until 2016 when Konceptca was launched. One of the pioneers in Online Education, he believes in providing a learning experience which is NEAT, SMOOTH and AFFORDABLE.

He specializes in practical subjects – Accounting, Costing, Taxation, Financial Management. With over 12 years of teaching experience (Online as well as Offline), he SURELY KNOWS IT ALL.

"Koncept perfectly justifies what it sounds, i.e, your concepts are meant to be cleared if you are a Konceptian. My experience with Koncept was amazing. The most striking experience that I went through was the the way Yash sir and Ruchika ma'am taught us in the lectures, making it very interesting and lucid. Another great feature of Koncept is that you get mentor calls which I think drives you to stay motivated and be disciplined. And of course it goes without saying that Yash sir has always been like a friend to me, giving me genuine guidance whenever I was in need. So once again I want to thank Koncept Education for all their efforts."

"Hello everyone, I am Kaushik Prajapati. I recently passed my CA Foundation Dec 23 exam in first attempt, That's possible only of proper guidance given by Yash sir and Ruchika ma'am. Koncept App provide me a video lectures, Notes and best thing about it is question bank. It contains PYP, RTP, MTP with soloution that help me easily score better marks in my exam. I really appericiate to Koncept team and I thankful to Koncept team."

"Hi. My name is Arka Das. I have cleared my CMA Foundation Exam. I cleared my 12th Board Exam from Bengali Medium and I had a very big language problem. Koncept Education has helped me a lot to overcome my language barrier. Their live sessions are really helpful. They have cleared my basic concepts. I think its a phenomenal app."

"I cleared my foundation examination in very first attempt with good marks in practical subject as well as theoretical subject this can be possible only because of koncept Education and the guidance that Yash sir has provide me, Thank you."