Accounting Fundamentals - Financial Accounting CMA Inter - CMA Inter syllabus

CMA Inter Blogs :

(100 Marks, Three Hours exam, 100% Descriptive Paper)

Learning Objective:

To gain understanding and to provide working knowledge of accounting concepts, detailed procedures and documentation involved in financial accounting system.

There are 9 Chapters in the CMA Inter Financial Accounting book. The chapters and their weightage are mentioned below.

| Exam Weightage | CMA Inter Financial Accounting subject Chapters |

|---|---|

| 15% |

Chp 1: Accounting Fundamentals |

| 10% | Chp 2: Bills of Exchange, Consignment, Joint Venture |

| 20% | Chp 3: Preparation of Final Accounts of Commercial Organisations, Not-for-Profit Organisations and from Incomplete Records |

| 20% | Chp 4: Partnership Accounting |

| 15% | Chp 5: Lease Accounting Chp 6: Branch (including Foreign Branch) and Departmental Accounts Chp 7: Insurance Claim for Loss of Stock and Loss of Profit Chp 8: Hire Purchase and Installment Sale Transactions |

| 20% | Chp 9: Accounting Standards |

According to Collins Dictionary, the term ‘framework’ refers to ‘a structure that forms a support or frame for something’. In the context of any system, it is ‘a particular set of rules, ideas, or beliefs which you use in order to deal with problems or to decide what to do’.

In accounting, ‘framework’ provides a common set of rules and guidelines that is used to measure, recognize, present, and disclose the information appearing in an entity’s financial statements.

Four Frameworks of Accounting

The framework of accounting has four pillars – Conceptual, Legal, Institutional and Legal. These are discussed below.

The Conceptual Framework is a body of interrelated objectives and fundamentals. The objectives identify the goals and purposes of financial reporting and the fundamentals are the underlying concepts that help achieve those objectives. Those concepts provide guidance in selecting transactions, events and circumstances to be accounted for, how they should be recognized and measured, and how they should be summarized and reported. It states the objectives of General-Purpose Financial Reporting and the information provided by it. Conceptual Framework also guides on the qualitative characteristics that the financial statements must possess. Conceptual Framework often plays an important role in the development of Institutional Framework and assists preparers to develop consistent accounting policies when no accounting standard applies to a particular transaction or other event, or when a standard allows a choice of accounting policy.

b. Legal Framework

Businesses are often controlled by various statutes under which they are formed. For example, in India, partnership organisations are governed by Indian Partnership Act, 1932 or Limited Liability Partnership Act, 2008, co-operatives are controlled by the Co-operative Societies Act, 1912, companies are governed by the Companies Act, 2013. In addition, banks are controlled by Banking Regulation Act, 1949, insurance companies are under the Insurance Act, 1938, electricity companies are also governed by the Central Electricity Act, 2003. All these statutes (including various Rules framed under them) not only govern the administrative set up of these organisations, but also provide important guidelines regarding use of resources, financing and also on the maintenance of books of accounts and treatment of pecified transactions. For example, the Companies Act, 2013 and Companies (Accounts) Rules, 2014 provide useful provisions on maintenance of accounting records, accounting for issue and redemption of securities, investments to be done, consolidation and even winding up of the company. Companies (Corporate Social Responsibility) Rules, 2014 provides the guidelines regarding accounting of CSR expenses as well as carry forward and set-off of excess amount spent. Thus, legal framework plays an important role in accounting. The Schedules of this Act also provide important guidelines on the form and contents of financial statements.

c. Institutional Framework

Institutional framework refers to the guidelines issued in form of certain pronouncements by institutionsentrusted by the sovereign authorities to oversee the development of the respective field. In India, the Institute of Chartered Accountants of India has been entrusted to develop standards in the field of accounting

to ensure comparability and consistency in accounting information. The Indian Accounting Standard Board of ICAI thus develops quality accounting standards on different areas of accounting. Currently, there are two sets of accounting standards in India – Accounting Standards as per Companies (Accounting Standards)

Rules, 2021 and Ind ASs under Companies (Indian Accounting Standards) Rules, 2015. In addition, the Cost Accounting Standards Board (CASB) of the Institute of Cost Accountants of India has, so far, developed 24 Cost Accounting Standards to facilitate cost accounting and reporting.

d. Regulatory Framework

The activities of organisations often come under the regulatory ambit of various regulators. In India, there are different regulatory authorities in different segments of financial market, such as RBI in money market operations, SEBI in capital market operations, IRDAI in insurance sector, PFRDA in pension funds. In addition, there are Telecom Regulatory Authority of India (TRAI), Competition Commission etc. The regulations imposed by these authorities may also have important bearing on accounting of a concerned entity. For example, regulations issued by SEBI largely shape the accounting and, more importantly, reporting by a listed firm in India. Similarly, regulations framed by IRDAI affect the accounting and reporting in insurance companies. In banking, BASEL Norms and other guidelines issued by RBI largely determine the accounting of NPA (Non-Performing Assets). Central Electricity Regulatory Commission (Terms and Conditions of Tariff) Regulations, 2009 affect the determination of tariff and accounting in an electricity company in India.

The above four frameworks provide the foundation on which accounting and more specifically corporateaccounting is based in India. They help to streamline the accounting process and help to improve the quality of the reports generated and thereby contribute in the overall development of accounting.

The responsibility of the discipline of accounting is to provide financial information to the users of accounting information. For this purpose, it keeps records of the various transactions in its books of accounts. The practice of record keeping may be practiced differently by different organisations. In order to ensure uniformity and consistency in record keeping, the accounting profession has developed rules, conventions, standards, and procedures which are generally accepted and universally practiced. This common set of rules, conventions, standards, and procedures is referred to as Generally Accepted Accounting Principles (GAAP).

The GAAPs indicate how to report economic events and are thus, used by organisations in drafting their financial statements. They are to be followed by organisations so that the users of accounting information have an optimum level of consistency in the financial statements they use, when analyzing companies for investment purposes.

Such accounting principles have been developed from research, accepted accounting practices, and pronouncements of regulators.

In India, financial statements are prepared on the basis of accounting standards issued by the Institute of Chartered Accountants of India (ICAI) and the law laid down in the respective applicable statutes (like, Schedule III to Companies Act, 2013 is required to be followed by all companies).

Concept of Accounting Principles, Accounting Concepts, and Accounting Conventions

Accounting Principles are the basic rules which act as a primary standard for recording business transactions and maintaining books of accounts. They provide standards for scientific accounting practices and procedures. They guide as to how the transactions are to be recorded and reported. They assure uniformity and understandability. Accounting principles are accepted as such if they happen to be (1) objective (2) usable in practical situations (3) reliable (4) feasible (they can be applied without incurring high costs); and (5) comprehensible to those with a basic knowledge of accounting and finance.

The accounting principles can be split into – [A] Accounting Concepts and [B] Accounting Conventions.

[A] Accounting Concepts refer to the assumptions and conditions that define the parameters and constraints within which the accounting operates. They lay down the foundation for accounting principles, and ensure recording of financial facts on sound bases and logical considerations. The common accounting concepts are:

(a) Entity Concept

(b) Going Concern Concept

(c) Periodicity Concept

(d) Money Measurement Concept

(e) Accrual Concept

(f) Dual Aspect Concept

(g) Matching Concept

(h) Realisation Concept

(i) Cost Concept

[B] Accounting Conventions are customs, methods, procedures or guidelines associated with the practical application of accounting principles. These are widely accepted, and are the common practices which are used as a guideline when recording transactions. Accounting conventions are a necessary part of the accounting

profession, since they result in transactions being recorded in the same way by multiple organizations. This allows for the reliable comparison of the financial facts and figures. However, accounting conventions may change over a period of time, thus reflecting shifts in the general opinion and/ or practice of dealing with a transaction. The different accounting conventions are:

(a) Convention of Conservatism

(b) Convention of Consistency

(c) Convention of Materiality

(d) Convention of Full Disclosure.

Accounting Concepts

(a) Entity Concept: As per this concept, an organisation is treated as distinct and separate from the persons who own or manage it. In other words, this concept assumes that the organization and business owners are two independent entities. Hence, the personal transaction of its owner is different from the transactions of the organisation. Application of this concept enables recording of transactions between the entity and its owners and/ or other stakeholders. The entity concept requires that all the transactions are to be viewed, interpreted and recorded from organisation’s point of view.

For example, if the owner pays his personal expenses from business cash, this transaction can be recorded in the books of business entity. This transaction will take the cash out of business and also reduce the obligation of the business towards the owner.

(b) Going Concern Concept: The basic assumption of this concept is that an organisation is assumed to continue to exist for an indefinite period of time. This simply means that every concern has continuity of life. Unless, there is good evidence to the contrary, the accountant assumes that an organisation is a ‘going concern’. This concept enables the accountant to carry forward the values of assets and liabilities from one accounting period to the other without asking the question about usefulness and worth of the assets and recoverability of the receivables. The going concern concept forms the basis for preparation of Balance Sheet of an organisation.

(c) Accounting Period Concept: Accounting period concepts assumes that the infinite life of an organisation can be split into smaller periods of equal duration (viz. a quarter, half-year or year). Due to this concept, the operating results are ascertained for a specific period, the financial position is reflected (through the balance sheet) at regular intervals.

(d) Money Measurement Concept: Any event which can be expressed in terms of money is always recorded in the books of accounts. The advantage of this concept is that different types of transactions could be recorded as homogenous entries with money as common denominator. A business may own ₹ 3 Lacs cash, 1500 kg of raw material, 10 vehicles, 3 computers etc. Unless each of these is expressed in terms of money, the assets owned by the business cannot ascertained. When expressed in the common measure of money, transactions could be added or subtracted to find out the combined effect. However, the limitation of this concept is that only the absolute value of the money is considered, whereas the real value may fluctuate from time to time due to inflation, exchange rate changes, etc.

(e) Accrual Concept: This concept is based on recognition of both cash and credit transactions. In case of a cash transaction, owner’s equity is instantly affected as cash either is received or paid. In a credit transaction, however, a mere obligation towards or by the organisation is created. When credit transactions exist (which is generally the case), revenues are not the same as cash receipts and expenses are not same as cash paid during the period.

(f) Dual Aspect Concept: The dual aspect concept assumes that every transaction recorded in the books of accounts is based on two aspects (technically called ‘Debit’ and ‘Credit’). This concept provides the basis for recording business transactions in the books of accounts. This implies that the transaction that is recorded affects two (or more) accounts on their respective opposite sides. Hence, the transaction should be recorded in atleast two accounts. For example, goods purchased in cash have two aspects such as ‘paying cash’ and ‘receiving goods’. Such duality of the transaction is commonly expressed in the terms of an equation as: Assets = Liabilities + Capital.

(g) Matching Concept: This concept states that the revenues and expenses must be recorded at the same time at which they are incurred. In general, the revenues earned should be matched with the expenses incurred during the accounting period. For the application of this concept several adjustments are made for prepaid expenses, accrued incomes, etc. The operating result of an accounting period can be measured only when incomes are compared with the related expenses incurred.

(h) Realisation Concept: The concept of realisation talks about how much of the revenue should be recognized in the books of accounts. It says, amount should be recognized only to the tune of which it is certainly realizable. Thus, mere getting an order from the customer won’t make it eligible to be recognized as revenue. The reasonable certainty of realizing the money will come only when the goods ordered are actually supplied to the customer and he is billed. This concept ensures that any income which is unearned or unrealized will not be considered as revenue.

(i) Cost Concept: The cost concept states all the business assets should be written down in the book of accounts at the costs incurred for their acquisition, including any capital cost incurred in relation to installation. The assets are not to be recorded at their market price. For example, a packing machine was purchased by Bharat Ltd. for ₹ 40,00,000. An amount of ₹ 30,000 was spent on transporting the machine to the factory site, and further ₹ 20,000 was additionally spent on its installation. Hence, the total amount at which the machine will be recorded in the books of accounts would be the aggregate of all these costs i.e. ₹ 40,50,000. This cost is also termed as ‘Historical Cost’.

Accounting Conventions

(a) Convention of Conservatism: The convention of conservatism essentially assumes an uncertain future and as such, advocates providing for all possible losses, but never for possible future gains. As such, application of this convention would always result in understatement of incomes, profits and thus, resources.

(b) Convention of Consistency: This convention advocates the continuous observation and application of the rules and practices of accounting. The uniformity and consistency of accounting rules is vital to profit and loss calculations as well as comparisons of company performance. Frequent changes in the treatment of accounts would result in inconsistency and hence, make the accounting information less reliable. It would result in making accounting information truthful, accurate and complete.

(c) Convention of Materiality: The convention of materiality advocates the recording and reflection of all material facts (i.e. those pieces of information that can potentially influence the decision of informed investor) in the accounting records, and elimination of insignificant information. It should be noted that any item of fact which is considered material by on organisation may be treated as unimportant by another organisation. In the same way, an item that is considered material during a particular time period may be treated as unimportant in subsequent time periods.

(d) Convention of Full disclosure: This convention advocates the full disclosure of all material information, whether favourable or otherwise, in the accounting statements of a business enterprise. This convention requires that all accounting statements must be prepared honestly. The convention of disclosure holds greater importance in the case of businesses where the ownership is separate from the management.

Conclusion

Accounting principle, concepts and conventions are very vital to the accounting profession, since they bring about uniformity in the process of recording transactions. Such uniformity makes it possible to reliably compare the financial results, financial position, and cash flows of different organizations and also over different periods. These, thus go a long way in helping to standardize the financial reporting process.

Proper distinction between transactions of capital and revenue nature is one of the fundamental requirements

of accounting. It is very significant as without this being done properly, the very objective of accounting

gets affected. The application of accounting concepts of periodicity, accrual and matching leads to the

identification of a transaction as either capital natured transaction or revenue natured transaction.

When transactions get properly classified between capital and revenue nature, it achieves the following purposes:

1. Ensures proper accounting of transactions by identifying them either as income or as liability, and expense

or asset;

2. Determination of true operating result by correct identification of incomes and expenses;

3. Proper disclosure of financial position in the balance sheet of the entity by correct disclosure of its assets and

liabilities.

After the incurrence of an expenditure by an entity, that expenditure has to be recognized as either a capital expenditure or a revenue expenditure before being recorded in the books of accounts.

Capital Expenditure refers to that expenditure, benefit from which can be enjoyed by an entity over a number of accounting periods. This type of expenditure happens to be non-recurring in nature. A capital expenditure takes place when an asset or service is acquired or improvement of a fixed asset is affected. These assets resulting from such expenditure are not intended for resale in the ordinary course of business.

Example: Purchase of machinery; Construction of building; Development of website; Heavy repairs of a noncurrent asset etc.

Accounting Treatment: An expenditure of capital nature is not written off completely (i.e. charged) against income in the accounting period in which it is acquired. Rather, it is capitalised (i.e. recorded) as an asset and gets reflected in the balance sheet. However, over time the amount of capital expenditure sliced for being recognized as revenue expenditure i.e. it gets gradually charged against the profit. For example, the acquisition of a machinery is a capital expenditure, but charging regular depreciation on this machinery is a revenue expenditure.

Revenue Expenditure refers to that expenditure, benefit from which can be enjoyed by an entity in the current accounting period. This type of expenditure happens to be recurring in nature. Revenue expenditures are incurred to carry on the regular course of operations by an organisation.

Example: Purchase of goods for sale; payment of recurring expenses (like salaries, wages, rent, depreciation, conveyance charges, monthly internet charges etc.); Repairs and maintenance of non-current assets etc.

Accounting Treatment: An expenditure of revenue nature charged as an expense against profit of the accounting period in which it is incurred or recognised.

The following are the points of distinction between Capital Expenditure and Revenue Expenditure:

| Capital Expenditure | Revenue Expenditure |

| The economic benefits from capital expenditure are enjoyed for more than one accounting period. | The economic benefits from revenue expenditure are enjoyed for only one accounting period. |

| It is non-recurring in nature. | It is recurring in nature. |

| Normally, it involves heavy cash outlay. | Normally, it involves lower cash outlay. |

| It is reflected in the Balance Sheet. | It is debited to Income Statement. |

| It may be incurred before or after the commencement of operations of an entity. | It is always incurred after the commencement of operations of an entity. |

| It tends to increase the earning capacity or, reduce the operating expenses of an entity. | It helps in carrying on the activities in the current accounting period. |

| A portion of capital expenditure may get matched against the revenue to determine the operating result. | Entire amount of such expenditure is matched against the revenue to determine the operating result. |

Certain Rules for Identification of Capital Expenditure

An expenditure can be recognised as capital if it is incurred for the following purposes:

Deferred Revenue Expenditures

Deferred Revenue Expenditure is the expenditure for which payment has been made or a liability has been incurred but which is carried forward on the presumption that will be of benefit over a subsequent period or periods. [As per guidance Note on Terms used in Financial Statements issued by Institute of Chartered Accountants of India]. Deferred revenue expenditures are a combination of capital and revenue expenses whose usefulness does not expire in the year of their occurrence, but generally expires in the near future. These type of expenditures are carried forward and are written-off in future accounting periods. A portion of such expenditure is capitalised even though it is revenue in nature, and hence is also referred to as Capitalised Revenue Expenditure.

Example: Heavy advertisement expenditure incurred prior to launching a new product; Development expenses of a product etc.

Accounting Treatment: A part of such expenditure (the expense portion) is recorded in the debit-side of the Income Statement, while the unwritten-off portion appears as an asset in the Balance Sheet.

NB: After the issuance of AS-26, the expenditures which were recognised as deferred revenue expenditure has to be treated as simple revenue expense. The accounting standard has specifically mentioned that any expenditure incurred for research, training, advertising and promotional activities should be recognised as an expense of the accounting period in which it has been incurred.

A receipt of money may be of a capital or revenue nature depending upon the source of the receipt. A clear distinction should be made between capital receipts and revenue receipts to ensure proper determination of operating results.

Capital Receipts refer to the receipts which are obtained by an entity from operations other than the regular operations of the entity. Capital receipts do not have any effect on the operating result (i.e. profits earned or losses incurred) during the course of a year.

Example: Additional capital introduced by proprietor/ partners; receipts from issue of fresh shares, by a company; proceeds from sale of long-term assets etc.

Accounting Treatment: Such receipt is credited to the respective account of capital nature, and gets reflected in the Balance Sheet.

Revenue Receipts refer to the receipts which are obtained by an entity from its regular course of operations. Receipts of money in the revenue nature increase the profits or decrease the losses of a business and must be set against the revenue expenses in order to ascertain the profit for the period.

Example: Collection from customers for goods sold on credit; Fees received for services rendered in the ordinary course of business; Recovery from customers earlier written-off as bad etc.

Accounting Treatment: These are recognised as income and should be credited to the Income Statement.

The following are the points of difference between capital receipts and revenue receipts:

| Capital Receipt | Revenue Receipt |

| These receipts are obtained by an entity from operations other than from the regular operations | These receipts are obtained by an entity from regular day-to-day operations. |

| It is not recognised as an income. | It is recurring in nature. |

| Normally, it involves heavy cash outlay. | It is recognised as an income. |

| It gets reflected in the Balance Sheet. | It is credited to Income Statement. |

| It does not affect the operating result of an entity. | It affects the operating result of an entity. |

| It may result in creation of liability. | It does not create any liability. |

The matching of revenues and expenses result in either profit or loss. As such, an extension of the discussion on expenditures and receipts of capital and revenue nature naturally leads to the concepts of ‘Capital and Revenue Profits’ and ‘Capital and Revenue Losses’.

While ascertaining the operating result of an entity in relation to an accounting period, proper distinction is to be made between capital profits and revenue profits.

Capital Profit refers to a profit which arises out of the non-operating activities of an entity. It is non-recurring in nature. Generally, capital profits arise out of the sale of assets other than inventory, or in connection with the raising of capital or at the time of purchasing an existing business.

Examples: Profit prior to incorporation; Premium received on issue of shares; Profit made on re-issue of forfeited shares; Redemption of Debenture at a discount; Profit made on sale or revaluation of a non-current tangible asset etc.

Accounting Treatment: Capital profits are generally capitalised i.e. transferred to a Capital Reserve Account. Revenue Profit refers to a profit which arises out of the regular operating activities of an entity. It is recurring in nature.

Example: Profit arising out of the sale of the merchandise that the business deals in; Profit made by rendering regular services to clients; Surplus earned by a non-profit organisation etc.

Accounting Treatment: Revenue profits, which get determined in the Income Statement, are distributed to the owners of the business or transferred to any Reserve Account.

While ascertaining losses, revenue losses are differentiated from capital losses, just as revenue profits are distinguished from capital profits.

Capital Loss refers to a loss which does not arise to an entity in the regular course of its operations.

Example: Capital losses may result from the sale of assets other than inventory for less than written down value; Diminution/ elimination of assets other than as the result of use or sale i.e. from extra-ordinary activities (viz. loss by flood, fire etc.) or in connection with raising debt capital by a company (issue of debentures at a discount) or on the settlement of liabilities for a consideration more than its book value (debenture issued at par but redeemed at a premium).

Accounting Treatment: It is either charged against the revenue i.e. debit-side of Income Statement or reflected in the asset-side of Balance Sheet (as fictitious assets). Revenue Loss arise to an entity from the normal course of business.

Example: Discount allowed to customers for prompt payment; loss due to bad debts etc.

Accounting Treatment: Such loss is to be recorded in the debit-side of Income Statement.

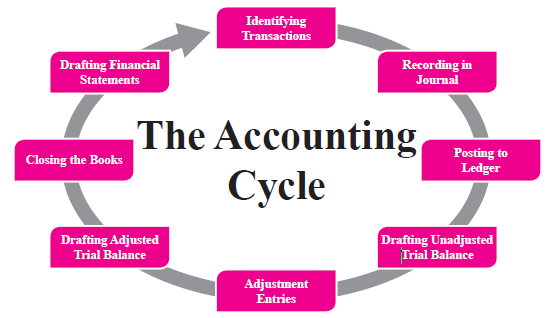

The Accounting Cycle is a sequence of activities performed by an accountant to document and report an organisation’s financial transactions during an accounting period. This cycle follows financial transactions from when they occur to how they affect financial documents. The entire process starting with identification of transactions, their recording and processing all transactions of an organisation, to its representation on the financial statements, and also to closing the accounts, if applicable, is referred to as Accounting Cycle. To keep track of the full accounting cycle from start to finish is one of the main duties of a bookkeeper.

Stages of Accounting Cycle

The accounting cycle consists of the following sequential steps:

1. Identifying transactions: The first step in the accounting cycle is to analyze events to determine if they are “transactions”. Transactions are the starting point from which the rest of the accounting cycle will follow.

2. Recording transactions in Books of Original Entry: The second step in the accounting cycle is to record the identified transactions in the relevant Books of Original Entry as journal entries.

3. Posting to the ledger: The next step is to record a summary of the activities in relevant account in the ledger (referred to as Posting).

4. Drafting of Unadjusted Trial Balance: At the end of an accounting period, data from the ledger accounts may be taken to draft a trial balance. It is prepared for identifying any errors that may have occurred during the initial stages of the accounting cycle. However, this step is not mandatory.

5. Passing of adjustment entries: Identification of necessary adjustments and passing of adjusting entries make up the fifth step in the cycle.

6. Drafting of Adjusted Trial Balance: Once all adjusting entries are completed, then an Adjusted Trial Balance can be prepared.T his happens to be the last step before the preparation of the financiatle msteants.

7. Closing of books: In this stage of the accounting cycle, the ledger accounts are closed and balanced (also referred to as “zeroed out”) at the end of every accounting period.

8. Drafting the Financial Statements: In the last stage of the accounting cycle, the Income Statement is prepared with the closing balances of the nominal accounts, while the balances of real and personal accounts gets reflected in the Balance Sheet.Financial statements are prepared in the following order: Income Statement, Statement of Retained Earnings, Balance Sheet and Statement of Cash Flows.

Events & Transactions

The primary purpose of financial accounting is to record the transactions entered into by an organisation during an accounting period. So, transactions are the staring point of the accounting cycle.Transactions are created through events, but all events are not transactions.

Events: Everything that is happening in every moment of human life is an event. Simply stated, any happening is an event. As such, events can be financial (like, purchasing a book, paying cab fare, receiving a cheque etc.) and non-financial (like, visiting a book store, going for morning walk etc.). An event may involve any number of parties, and may be complete and may be incomplete.

Transactions: An accounting transaction is an event which has a monetary impact on the financial position of the organisation. In order to be considered as a transaction, an event has to satisfy the following conditions:

1. It must be measurable in terms of money.

2. It must involve atleast two parties.

3. It involves a monetary exchange for a goods or service.

4. It must cause a change in the financial position of the entity.

Analysis of Transactions

An organisation enters into various transactions during the course of its operations. These transactions cause changes in financial position of the organisation. Analysis of transactions implies observing the changes in financial position of the organisation caused by the transactions entered into by it during an accounting period. A change in financial position means change in one or more of the five basic elements of accounting, they being: Assets, Liabilities, Capital/ Equity, Expenses, and Revenue.

In the following example of a trading proprietorship business, various illustrative transactions are used to understand the changes in different elements of accounting

| Transaction 1: Mr. Suman De commences his business by investing ₹ 5,00,000 in cash. |

| Changes brought about by this transaction are: |

| Cash increases in the business by ₹ 5,00,000; (Element changed: Asset increase) |

| Capital increases by ₹ 5,00,000 (Element changed: Capital/ Equity increase) |

| Transaction 2: Mr. De opened a current account with the bank by depositing ₹ 2,00,000. |

| Changes brought about by this transaction are: |

| Cash balance decreases by ₹ 2,00,000; (Element changed: Asset decrease) |

| Bank balance increases by ₹ 2,00,000 (Element changed: Asset increase) |

| Transaction 3: He borrows ₹ 1,20,000 from bank interest @ 10% p.a. |

| Changes brought about by this transaction are: |

| Bank balance increases by ₹ 1,20,000 (Element changed: Asset increase); |

| Bank loan increases by ₹ 1,20,000 (Element changed: Liability increase) |

| Transaction 4: Mr. De purchases equipments worth ₹ 80,000 for cash. |

| Changes brought about by this transaction are: |

| Equipments increase by ₹ 80,000; (Element changed: Asset increase) |

| Cash decrease by ₹ 80,000 (Element changed: Asset decrease) |

| Transaction 5: He purchased goods worth ₹ 1,00,000 for resale, out of which 60% was paid in cash, 30% by cheque and balance was due. |

| Changes brought about by this transaction are: |

| Purchases increases by ₹ 1,00,000; (Element changed: Expenses increase) |

| Cash balance decreases by ₹ 60,000 (Element changed: Asset decrease) |

| Bank balance decreases by ₹ 30,000 (Element changed: Asset decrease) |

| Creditors/ Payables increases by ₹ 10,000 (Element changed: Liability increase) |

| Transaction 6: Goods sold in cash ₹ 1,70,000. |

| Changes brought about by this transaction are: |

| Cash increases by ₹ 1,70,000; (Element changed: Asset increase) |

| Sales increase by ₹ 1,70,000 (Element changed: Revenue increase) |

| Transaction 7: Goods sold on credit for ₹ 80,000. |

| Changes brought about by this transaction are: |

| Debtors/ Receivables increases by ₹ 80,000 (Element changed: Asset increase) |

| Sales increase by ₹ 80,000 (Element changed: Revenue increase) |

| Transaction 8: Mr. De incurred ₹ 20,000 as wages. |

| Changes brought about by this transaction are: |

| Wages increases by ₹ 20,000; (Element changed: Expenses increase) |

| Cash decreases by ₹ 20,000 (Element changed: Asset decrease) |

| Transaction 9: Interest on bank loan charged ₹ 3,000. |

| Changes brought about by this transaction are: |

| Bank interest increased by ₹ 3,000; (Element changed: Expenses increase) |

| Bank balance decreased by ₹ 3,000 (Element changed: Asset decrease) |

| Transaction 10: He collected cash ₹ 20,000 from his customer. |

| Changes brought about by this transaction are: |

| Cash increases by ₹ 20,000; (Element changed: Asset increase) |

| Debtors/ Receivables decreases by ₹ 20,000 (Element changed: Asset decrease) |

| Transaction 11: Mr. De paid ₹ 8,000 to his supplier. |

| Changes brought about by this transaction are: |

| Cash decreases by ₹ 8,000; (Element changed: Asset decrease) |

| Creditors/ Payables decreases by ₹ 8,000 (Element changed: Liability decrease) |

| Transaction 12: He withdrew cash ₹ 7,000 for his personal use. |

| Changes brought about by this transaction are: |

| Cash decreases by ₹ 7,000; (Element changed: Asset decrease) |

| Capital decreases by ₹ 7,000 (Element changed: Capital/ Equity decrease) |

Such analysis of the transactions helps in identification of the accounts which would be involved for accounting purposes and also helps in identification of the debit and credit aspects of every transaction.

The primary purpose of financial accounting is to record the transactions entered into by an organisation during an accounting period. To achieve this, various accounts are opened and after the classification exercise the transactions get posted in the ledger (which itself is classified as personal and impersonal). These happen to be the building blocks for developing the financial statements and other management reports of the organisation.

However, with the increase in the complexity of business and flow of data, it has become quite a challenge to retrieve the information stored in the accounting records. It is for the purpose of effective management and retrieval of the already recorded accounting information, Chart of Accounts are developed and they are codified.

Charts of Accounts

Codification Structure

Illustration of Account Codification for a small business organisation:

For a small business, three digits code may suffice for the account number, although more digits are desirable. However, in order to allow for new accounts to be added as the business grows with more digits, new accounts can be added while maintaining the logical order. Complex businesses may have thousands of accounts, and require longer account reference numbers.As such, it is worthwhile to put thought into assigning the account numbers in a logical way and to follow any specific industry standards.

The following is an example of some of the accounts that may be included in a chart of accounts and reflecting how the digits might be coded:

| Account Numbering & Description of Accounts |

| 1000 to 1999: Asset accounts |

| 2000 to 2999: Liability accounts |

| 3000 to 3999: Equity accounts |

| 4000 to 4999: Revenue accounts |

| 5000 to 5999: Cost of goods sold accounts |

| 6000 to 6999: Expense account |

| 7000 to 7999: Other revenue (for example rent received, bad debt recovery etc.) |

| 8000 to 8999:Other expenses (for example depreciation income taxes etc.) |

An alternative presentation of a typical Chart of Accounts is as follows:

| Balance Sheet Accounts | Income Statement Accounts |

| Assets (1000 – 1999) | Operating Revenues (4000 – 4999) |

| Liabilities (2000 – 2999) | Operating Expense (5000 – 5999) |

| Owner’s Equity (3000 -3999) | Overhead Costs or Expenses (6000 – 6999) |

| Non-operating revenue and gains (7000 – 7999) | |

| Non- operating expenses and Losses (8000 – 8999) |

It is to be noted that by separating each account by several numbers many new accounts can be added between any two while maintaining the logical order.

Accounting Equation

The accounting equation is a representation of how the three important components of accounting namely Assets,Liabilities and Equity are associated with each other.

In the most simplistic form, the accounting equation is presented as: Assets = Liabilities + Equity.

Assets represent the valuable resources controlled by the companysuch as cash, accounts receivable, fixed assets, inventory etc. Liabilities represent its obligations of an organisation to its external stakeholders, while Equity represents owners net claim on the assets. It is to be noted that, the liabilities and equity represent how the assets of the organisation has been financed.

All three components of the accounting equation appear in the balance sheet, which reveals the financial position of an entity at any given point in time.

Expanded Accounting Equation: The above equation can be further expanded by incorporating the various elements of the Equity component as under:

Assets = Liabilities + Equity

or, Assets = Liabilities + [Capital + (Revenue – Expenses) – Drawings]

or, Assets + Expenses + Drawings = Liabilities + Capital + Revenue

This equation is considered to be the foundation of the double-entry accounting system. At a general level, this means that whenever there is a recordable transaction, the choices for recording it all involve keeping the accounting equation in balance.

Illustrative Accounting Equation Transactions

The following table shows a few of the common accounting transactions and their recording within the framework of the accounting equation:

| Transaction | Assets + Expenses + Drawings | Liabilities + Capital + Revenue |

| Cash introduced by proprietor | Cash (Assets) increases | Capital increases |

| Purchase of goods in cash | Inventory (Asset) increases; Cash (Assets) decreases | N.A. |

| Purchase of goods in credit | Inventory (Asset) increases | Creditors/ Payables (Liabilities) increases |

| Sale of goods in cash | Cash (Assets) increases; Inventory (Assets) decreases | N.A. |

| Sale of goods in credit | Debtors/ Receivables (Assets) increases; Inventory (Assets) decrease | N.A. |

| Salaries paid | Salaries (Expenses) increases; Cash/ Bank (Assets) decreases | N.A. |

| Rent received | Cash/ Bank (Assets) increases | Rent received (Revenue) increases |

| Goods withdrawn by proprietor | Inventory (Assets) decreases | Capital decreases |

Double Entry System

Double Entry System of Bookkeeping is an accounting system which recognizes the fact that every transaction has two aspects and both aspects of the transaction are recorded in the books of accounts.It is a fundamental concept encompassing accounting and book-keeping in present times.

Double entry system records the transactions by understanding them as a Debit item or Credit item. A debit entry in one account gives the opposite effect in another account by credit entry. This means that the sum of all Debit accounts must be equal to the sum of Credit accounts.

This system is based on the accounting equation and requires:

1. Every business transaction to be recorded in at least two accounts.

2. The total debits recorded for each transaction to be equal to the total credits recorded.

Rules of Debit and Credit under Double Entry System

The double-entry accounting system is based on specific rules of debit and credit for recording transactions in the accounts. The rules of debit and credit can be explained by applying two methods:

1. Golden Rules; and

2. Accounting Equation

Successive Processes of the Double Entry System

Books of Original Entry& Subsidiary Books

Types of Books of Original Entry

The books of original entry are broadly classified into two categories:– Special Journals (Day Books) and General Journal. (Refer to para 1.5- Types of Journal).

Posting in Ledger & Finalization of Accounts

The first step in the accounting cycle, after the identification of transactions happens to be recording of transactions in the journal, followed by their posting in respective accounts in the ledger.

Journal

Journal is the book of original entry in which financial transactions are firstly recorded after their occurrence in chronological order. It is in this book of accounts where the transactions are recorded in the first place.

The word ‘Journal means’ a daily record. Journal is derived from French word ‘Jour’ which means a day. This book of account is also referred to as the Book of Prime Entry or Books of First Entry.

The process of recording the transactions in a journal is called ‘Journalizing’. This is the first activity that a book-keeper performs after identification of the transactions which has to be recorded in the books of accounts of a concern.

The entry made in this book is called a ‘Journal Entry’. Every entry in the journal is followed by a short summary which describes the particular transaction. This short summary is referred to as ‘Narration’. Every entry in the book of original entry must be followed by such a narration.

Example of a Transaction and its Journal Entry:

As per voucher no. 31 of Roy Brothers, on 09.02.2022 goods of ₹ 50,000 <.a>were purchased. Cash was paid immediately. The folios of the Purchase A/c and Cash A/c in the ledger are 5 and 17 respectively. Journal entry of the above transaction is given below:

| Date | Particulars | Voucher No. |

Ledger Folio |

(₹) | (₹) |

| 09.02.2022 | Purchase A/c Dr. | 31 | 5 | 50,000 | |

| To Cash A/c (Being goods purchased for cash) | 17 | 50,000 |

Types of Journal

The books of original entry are broadly classified into two categories:

1. Special Journal

A Special Journal is a book of primary entry in which transactions of a specific type viz. credit purchases, credit sales, return inwards etc. are first recorded before being posted in the respective ledger account. These are also referred to as Subsidiary Books. During the lifecycle of and organisation, when the volume of transactions increases to an extent that a single journal may no longer be adequate to record the transactions effectively, then special purpose books or subsidiary books are required for more efficient record keeping purposes. The different special journals that are usually maintained by an organisation for primary recording of its transactions are:

(a) Cash Journal or Cash Book is a special journal which is maintained for recording all transactions which involve cash, whether cash inflows or cash outflows.

(b) Purchase journal is a special journal which is used by an organization to record all the credit purchases made by it during an accounting period. It is also known as Purchase Book or Purchase Daybook.

(c) Sales Journal is a type of special journal that is used to record credit sale transactions of an organisation. It is also known as Sales Book or Sales Daybook.

(d) Purchase Return Journal is the special journal that is used for recording the goods which have been returned by an organisation to its suppliers, for any reason. It is also known as Purchase Return Book or Purchase Daybook.

(e) Sales Return Journal is the special journal that is used for recording the goods which have been returned to an organisation by its customers, for any reason. It is also known as Sales Return Book or Sales Daybook.

(f) Bills Receivable Journal is the special journal which is used to record the details of bills of exchange received by an entity from its customers during an accounting period. It is also known as Bills Receivable Book or Bills Receivable Daybook.

(g) Bills Payable Journal is the special journal which is used to record the details of bills of exchange accepted by an entity towards its suppliers during an accounting period. It is also known as Bills Payable Book or Bills Payable Daybook.

2. General Journal:

This is a book of original entry in which those transactions are recorded for which no specific day book is maintained are recorded.

In the following section, the important subsidiary books have been discussed.

1(a): Cash Journal or Cash Book

Cash Journal or Cash Book is a special journal which is maintained for recording all transactions which involve cash, whether cash inflows or cash outflows. In this book of original entry, transactions of every type (whether capital natured transactions or revenue natured transactions) are entered. This journal records the details of each transaction effected in cash by an organisation. Such details include the date, particulars, voucher number, ledger folio and the amount of the transaction.

The various aspects of the Cash Book has been discussed in detail in Para 1.6 of the study material.

1(b): Purchase Journal

The Purchase Journal is a book of original entry which is meant for recording credit purchase of goods. It is also known as Purchase Day Book or simply, Purchase Book. It is to be noted that cash purchases of goods are not recorded in this day book. Also purchase of other long term assets (like equipment, furniture, machinery etc.) on credit does not find place in purchase day book.

The Purchase journal records the details of the credit purchase of goods made by an organisation. Such details include the date of purchase, particulars of items purchased, inward invoice number, ledger folio and the amount of purchase.

The format of a purchase journal is as given below

| Date | Particulars | Inward Invoice no. | Ledger Folio No. | (₹) |

Source document for entry in purchase journal:

All entries in this book are made from the Purchase invoices. A purchase invoice is a statement which is issued by the seller of goods to the buyer of goods reflecting the details of the goods like the date of purchase, the quantity of purchase, the rate per unit, the total amount and also the terms of payment, if any.

Posting from Purchase Journal to Ledger

The Purchase Journal, being a book of original entry, transactions entered here are thereafter required to be posted to the respective ledger accounts in the ledger. The total of the purchases made during a period is posted to Purchases Account in the general ledger, while the individual credit purchase transactions posted in the personal ledger accounts of the respective suppliers (in the suppliers ledger)

1(c): Sales Journal

Sales Journal is the book of original entry which records credit sales of goods. It is also known as Sales Day Book or simply, Sales Book. It is to be noted that sale of goods for cash are not recorded in this day book. Also sale of other long term assets (like equipment, furniture, machinery etc.) does not find place in this book of original entry.

The Sales journal records the details of the credit sales of goods made by an organisation during a period. Such details include the date of sale, particulars of items sold, outward invoice number, ledger folio and the amount of sales.

The format of a typical sales journal is as given below:

| Date | Particulars | Outward Invoice no. | Ledger Folio No. | (₹) |

Source Document for Entry in Sales Journal:

All entries in this book are made from the Sales invoices. A sales invoice is a statement which is issued by the seller of goods to the buyer of goods reflecting the details of the goods like the date of sale, the quantity of sale, the rate per unit, the total amount and also the terms of payment, if any.

Posting from Sales Journal to Ledger

The Sales Journal, being a book of original entry, transactions entered here are thereafter required to be posted to the respective ledger accounts in the ledger. The total amount of sales made during a period is posted to Sales Account in the general ledger, while the individual entries of credit sale are posted in the personal ledger accounts of the respective customers/ debtors (in the debtors ledger).

1(d): Purchase Returns Journal

The Purchase Returns Journal is a book of original entry which is meant for recording returns of goods purchased on credit from the suppliers. It is also known as Returns Outward Day Book. It is to be noted that returns arising out of cash purchases of goods, or return of any assets other than merchandising goods on credit does not find place in this day book. The Purchase returns journal records the details of the returns arising out of credit purchase of goods viz. the date of return, particulars of items returned, name of supplier, debit note number, ledger folio and the total amount.

The format of a purchase returns journal is as given below

| Date | Particulars | Debit Note no. | Ledger Folio No. | (₹) |

Source Document for Entry in Purchase Returns Journal:

All entries in this book are made from the debit notes issued to respective suppliers or credit notes received from the respective suppliers.

Posting from Purchase Returns Journal to Ledger

The Purchase Returns Book, being a book of original entry, transactions entered here are thereafter required to be posted to the respective ledger accounts in the ledger. The total of the purchase returns made during a period is posted to Purchase Returns or Return Outwards Account in the general ledger, while the individual purchase return transactions posted in the personal ledger accounts of the respective suppliers (in the Creditors Ledger).

1(e): Sales Returns Journal

Sales Return Journal is the book of original entry which records returns of goods earlier sold on credit basis. It is also known as Sales Returns Day Book or simply, Sales Returns Book.

The Sales Returns Book records the details of the goods returned out of credit sales made by an organisation during a period. Such details include the date of return, particulars of items returned, credit note number, ledger folio and the amount of sales returns.

The format of the sales return journal is as given below

| Date | Particulars | Credti Note no. | Ledger Folio No. | (₹) |

Source Document for Entry in Sales Returns Journal:

All entries in this day book are made from the Credit Note issued by the seller of goods. A sales invoice is a statement which is issued by the seller of goods to the buyer of goods reflecting the details of the goods like the date of sale, the quantity of sale, the rate per unit, the total amount and also the terms of payment, if any.

Posting from Sales Returns Journal to Ledger

As the Sales Return Journal is a book of original entry, and so transactions recorded here are thereafter required to be posted to the respective accounts in the ledger. The total amount of sales returns made during a period is posted to Returns Inward (or Sales Returns) Account in the general ledger, while the individual entries of sale returns are posted in the personal ledger accounts of the respective customers/ debtors (in the Debtors ledger).

1(f): Bill Receivable Journal

The Bill Receivable Journal is a book of original entry which is meant for recording the bills of exchange received from the customers to whom goods have been sold on credit. This journal records the details like the details of the customer, name of drawer, name of acceptor, date of receipt of the bill, dae of drawing of the bill, date of acceptance of the bill, tenure of the bill, date of maturity, ledger folio and the amount of the bill.

Source document for entry in purchase journal:

All entries in this book are made from the bills of exchanges received from the customers.

Posting from Bill Receivable Journal to Ledger

The Bill Receivable Journal, being a book of original entry, transactions entered here are thereafter required to be posted to the respective ledger accounts in the ledger. The total of the bill of exchanges received during a period is posted to Bills Receivable Account in the general ledger, while the individual transactions posted in the personal ledger accounts of the respective customers (in the Debtors Ledger).

1(g): Bill Payable Journal

The Bill Payable Journal is a book of original entry which is meant for recording the bills of exchange issued to the suppliers from whom goods have been purchased on credit. This journal records the details like the details of the supplier, name of drawer, name of acceptor, date of issue of the bill, date of drawing of the bill, date of acceptance of the bill, tenure of the bill, date of maturity, ledger folio and the amount of the bill.

Source document for entry in purchase journal:

All entries in this book are made from the bills of exchanges issued to the suppliers.

Posting from Bill Payable Journal to Ledger

The Bill Payable Journal, being a book of original entry, transactions entered here are thereafter required to be posted to the respective ledger accounts in the ledger. The total of the bill of exchanges issued during a period is posted to Bills Payable Account in the general ledger, while the individual transactions posted in the personal ledger accounts of the respective customers (in the Creditors Ledger).

2. General Journal or Journal Proper

General Journal is the book of original entry in which those transactions for which no special journal is maintained are recorded. In other words, transactions like credit purchases, credit sales, purchase returns, sales returns etc. (for which specific subsidiary books are maintained) are recorded in this book of primary entry. This book of original entry is also known as Journal Proper. The following transactions are recorded in this book of original entry:

Types of Entries Recorded in Journal Proper

Opening entries: These entries are passed for bringing the balances of certain accounts in the books of the current accounting period. The different accounts whose balances are brought forwards are the assets, liabilities and equity accounts appearing the Balance Sheet of the preceding accounting period.

Transfer entries: In accounting, it is sometimes necessary to transfer an amount or balance of one account to some other account. The journal entries through which the amount of an account are transferred to another account are referred to as Transfer entries. Such entries are used when a wrong booking has been made in respect of any account or to allocate an expense/ revenue from one account to another.

Closing entries: All the expenses and gains or income related nominal accounts must be closed at the end of the year. The entries which are passed at the end of an accounting period for closing the nominal accounts by transferring them to the profit determining accounts like Trading Account, Profit & Loss Account, Consignment Account, Joint Venture Account, Income & Expenditure Account etc.

Adjustment entries: These entries are passed at the time of finalization of accounts for honouring the different generally accepted accounting principles i.e. accounting concepts and accounting conventions.

Rectification entries: These entries are passed for correcting the different errors that get committed while recording, posting, casting, balancing etc. in the books of accounts.

Rules of Journalising

Rules of Debit and Credit Based on the Types of Account(Golden Rules Approach)

| Nature of Account | Rule of Debit and Credit | |

| Nomial Account | Debit | Expenses and Losses |

| Credit | Incomes and Gains | |

| Real Account | Debit | What comes in |

| Credit | What goes out | |

| Personal Account | Debit | The receiver |

| Credit | The giver | |

Rules of Debit and credit Based on the Accounting Equation (Accounting Equation Approach)

Accounting equation is a statement of equality between the three basic elements of accounting viz. assets, liabilities and equity. Each and every financial transaction affects any one or more of these three basic elements. However, the total of all assets is always equal to the total of liabilities and equity at any point in time. The rules of debiting and crediting an account based on the accounting equation have been summarized hereunder:

| Components of Accounting Equation | Rule of Debit and Credit | |

| Assets | Debit | Increase |

| Credit | Decrease | |

| Laibilities | Debit | Decrease |

| Credit | Increase | |

| Capital | Debit | Decrease |

| Credit | Increase | |

| Drawings | Debit | Increase |

| Credit | Decrease | |

| Expenses | Debit | Increase |

| Credit | Decrease | |

| Revenue | Debit | Decrease |

| Credit | Increase | |

Steps in Journalising

The process of journalising involves the following steps:

1. Determination of the accounts involved in the transaction.

2. Classifying the accounts either as ‘Nominal, Real and Personal’ or into ‘Assets, Liabilities, Capital, drawings, Expenses and Revenue’.

3. Appling the rules of debit and credit for the identified accounts for identifying which account is to be debited and which accounts is to be credited.

4. Recording the details of the transaction viz. date, particulars and its narration, and also the amount to be debited and credited.

5. Writing a brief summary of the transactions (called narration) at the end.

Functions of Journal

The functions performed by the book of original entry are:

Advantages of Journal

The book of original entry provides the following advantages:

Limitations of Journal

Ledger

The book of account in which transactions are recorded in respective account, after they have been entered in the journal is called the Ledger. It is the book of account in which the transactions are recorded in a classified and permanent manner. It is the final destination of all the accounts, and hence, it is also called the Book of Final Entry. The process of recording the entry in the ledger is technically known as Posting. It is the book of account in which transactions are recorded from the journal. It contains various ‘ledger accounts’. The transactions are recorded in each of the relevant ledger accounts in a chronological order. It reflects the final position of each account on any particular date. It forms the basis for preparation of Trial Balance. . A ledger account has a specific format, as under:

………………. Account

| Date | Particulars | J.F. | (₹) | Date | Particulars | J.F. | (₹) |

Functions of Ledger

Subdivisions of Ledger

On the basis of the nature of accounts maintained, ledger can be classified into Personal Ledger and General Ledger.

1. Personal Ledger: The ledger which contains the personal accounts of the debtors and creditors is called Personal Ledger. It can be further sub-divided into:

(a) Debtors’/Customers’/Sales ledger: It contains the personal accounts of all the customers/trade debtors.

(b) Creditors’/Suppliers’/Purchase/Bought ledger: It contains the personal accounts of all the suppliers/ trade creditors.

2. Impersonal Ledger or General Ledger: The ledger which contains the accounts other than those contained in the ‘Personal Ledger’ is called Impersonal/General Ledger. The types of accounts maintained in this ledger are Real, Nominal and Personal (except Trade Debtors and Trade Creditors). The advantages of such sub-division are:

Ledger Posting

As and when the transaction takes place, it is recorded in the journal in the form of journal entry. This entry is posted again in the respective ledger accounts under double entry principle from the journal. This is called ledger posting.

The rules for writing up accounts of various types are as follows:

Assets: Increases on the left hand side or the debit side and decreases on the credit side.

Liabilities: Increases on the credit side and decreases on the debit side.

Capitals: The same as liabilities.

Expenses: Increases on the debit side and decreases on the credit side.

Incomes or Gains: Increases on the credit side and decrease on the debit side.

To summarise

| Dr. | Assets | Cr. |

| Increase | Decrease |

| Dr. | Liabilities & Capital | Cr. |

| Decrease | Increase |

| Dr. | Expenses or Loses | Cr. |

| Decrease | Increase |

| Dr. | Income or Gains | Cr. |

| Increase | Decrease |

Concepts of Debit and Credit

A debit denotes:

(a) In the case of a person that he has received some benefit against which he has already rendered some service or will render service in future. When a person becomes liable to do something in favour of the firm, the fact is recorded by debiting that person’s account : (relating to Personal Account)

(b) In case of goods or properties, that the value and the stock of such goods or properties has increased, (relating to Real Accounts)

(c) In case of other accounts like losses or expenses, that the firm has incurred certain expenses or has lost money. (relating to Nominal Account)

A credit denotes:

(a) In case of a person, that some benefit has been received from him, entitling him to claim from the firm a return benefit in the form of cash or goods or service. When a person becomes entitled to money or money’s worth for any reason. The fact is recorded by crediting him (relating to Personal Account)

(b) In the case of goods or properties, that the stock and value of such goods or properties has decreased. (relating to Real Accounts).

(c) In case of other accounts like interest or dividend or commission received, or discount received, that the firm has made a gain (relating to Nominal Account)

Balancing of Ledger Accounts

After all the transactions of a period get posted in the ledger, the net effect of these transactions is ascertained. This process of ascertaining the net effect of all the transactions posted in a particular ledger account for a period is called Balancing of a ledger account. The process of balancing an account involves totaling both the sides (i.e. debit side and credit side) of an account and ascertaining the difference between the two.

An account can show debit balance, or credit balance or nil balance. An account is said to be having a debit balance when its debit-side total is higher than the credit side total; while an account is said to have a credit balance when its credit-side total is higher than the debit-side total. When both side have same total, the account is said to have nil balance. This is very significant function of accounting as the finalization of accounts is done with the balances of the ledger accounts.

Illustration 1

For the following transactions pass the journal entries and post them in Ledger:

| 2022 |

| April 1 – Mr. Vikas and Mrs. Vaibhavi who are husband and wife start consulting business by bringing in their personal cash of ₹ 5,00,000 and ₹ 2,50,000 respectively. |

| April 10 – Bought office furniture of ₹ 25,000 for cash. |

| April 11 – Opened a Current Account with Bank of BB by depositing ₹ 1,00,000 |

| April 15 – Paid office rent of ₹ 15,000 for the month by cheque. |

| April 20 – Bought a motor car for ₹ 4,50,000 from Millenium Motors by making a down payment of ₹ 50,000 by cheque and the balance by taking a loan from HH Bank |

| April 25 – Vikas and Vaibhabi carried out a consulting assignment for AA Pharmaceuticals and raised a bill for ₹ 10,00,000 as consultancy fees. AA Pharmaceuticals have immediately settled ₹ 2,50,000 by way of cheque and the balance will be paid after 30 days. The cheque received is deposited into bank |

| April 30 – Salary of a receptionist at the rate ₹ 5,000 per month and an officer at the rate ₹ 10,000 per month the salary for the current month is payable to them. |

Solution:

Books of Vikas and Vaibhavi

Journal

| Date | Particulars | J.F. | V.N. | Dr.(₹) | Cr.(₹) |

| 2022 April 1 | Cash A/c……. Dr. | 7,50,000 | |||

| To, Vikas’s Capital A/c | 5,00,000 | ||||

| To, Vaibhavi’s Capital A/c (Being capital brought by the partner) | 2,50,000 | ||||

| April 10 | Furniturw A/c.... Dr. | 25,000 | |||

| To, Cash A/c (Being furniture purchased in cash) | 25,000 | ||||

| April 11 | Bank of BB A/c……. Dr. | 1,00,000 | |||

| To, Cash A/c (Being current account opened with Bank of BB) | 1,00,000 | ||||

| April 15 | Rent A/c. .... Dr. | 15,000 | |||

| To, Bank of BB A/c | 15,000 | ||||

| April 20 | Motor Car A/c. ...... Dr. | 4,50,000 | |||

| To, Bank of BB A/c Dr. | 50,000 | ||||

| To, Loan from HH Bank A/c(Being car purchased from Millenium Motors by making a down payment and Loan arrangements) | 4,00,000 | ||||

| April 25 | Bank of BB A/c……. Dr. | 2,50,000 | |||

| AA Pharmaceuticals A/c….. Dr. | 7,50,000 | ||||

| To, Consultancy Fees A/c (Being amount received and revenue recognized for fees charged) | 10,00,000 | ||||

| April 30 | Salary A/c………. Dr. | 15,000 | |||

| To, Salary Payable A/c (Being the entry to record salary obligation for the month.) | 15,000 |

LEDGER

Cash Account

| Date | Particulars | J.F. | (₹) | Date | Particulars | J.F. | (₹) |

| 1.4.22 | To, Vikas’s Capital A/c | 5,00,000 | 10.4.22 | By, Furniture A/c | 25,000 | ||

| 1.4.22 | To, Vaibhavi’s Capital A/c | 2,50,000 | 11.4.22 | By, Bank of BB A/c | 1,00,000 | ||

| 7,50,000 | 7,50,000 | ||||||

| 1.5.22 | To, Bal b/d | 6,25,000 |

Mr. Vikas's Capital Account

| Date | Particulars | J.F. | (₹) | Date | Particulars | J.F. | (₹) |

| 30.4.22 | To, Bal c/d | 5,00,000 | 1.4.22 | By, CashA/c | 5,00,000 | ||

| 1.5.22 | By, Bal b/d | 5,00,000 |

Mrs. Vaibhavi's Capital Account

| Date | Particulars | J.F. | (₹) | Date | Particulars | J.F. | (₹) |

| 30.4.22 | To, Bal c/d | 2,50,000 | 1.4.22 | By, CashA/c | 2,50,000 | ||

| 1.5.22 | By, Bal b/d | 2,50,000 |

Furniture Account

| Date | Particulars | J.F. | (₹) | Date | Particulars | J.F. | (₹) |

| 1.4.22 | To, Cash A/c | 25,000 | 30.4.22 | By, Bal b/d | 25,000 | ||

| 1.5.22 | To, Bal b/d |

Bank of BB Account

| Date | Particulars | J.F. | (₹) | Date | Particulars | J.F. | (₹) |

| 11.4.22 | To, Cash A/c | 1,00,000 | 30.4.22 | To, Bal b/d | 15,000 | ||

| 25.4.22 | To, Consultancy Fees A/c | 2,50,000 | 20.4.22 | By, Motor Car A/c | 50,000 | ||

| 30.4.22 | By, Bal c/d | 2,85,000 | |||||

| 3,50,000 | 3,50,000 | ||||||

| 1.5.22 | To, Bal b/d | 2,85,000 |

Rent Account

| Date | Particulars | J.F. | (₹) | Date | Particulars | J.F. | (₹) |

| 15.4.22 | To, Bank of BB A/c | 15,000 | 30.4.22 | By, Bal c/d | 15,000 | ||

| 1.5.22 | To, Bal b/d | 15,000 |

Motor Car Account

| Date | Particulars | J.F. | (₹) | Date | Particulars | J.F. | (₹) |

| 20.4.22 | To, Bank of BB A/c | 50,000 | 30.4.22 | By, Bal c/d | 4,50,000 | ||

| 20.4.22 | To, Loan from HH Bank A/c | 4,00,000 | |||||

| 4,50,000 | 4,50,000 | ||||||

| 1.5.22 | To, Bal b/d | 4,50,000 |

Loan from HDFC Bank

| Date | Particulars | J.F. | (₹) | Date | Particulars | J.F. | (₹) |

| 30.4.22 | To, Bal c/d | 4,00,000 | 20.4.22 | By, Motor Car A/c | 4,00,000 | ||

| 1.5.22 | By, Bal b/d | 4,00,000 |

Avon Pharmaceuticals Account

| Date | Particulars | J.F. | (₹) | Date | Particulars | J.F. | (₹) |

| 25.4.22 | To, Consultancy Fees A/c | 7,50,000 | 30.4.22 | By, Bal c/d | 7,50,000 | ||

| 7,50,000 |

Consultancy Fees Account

| Date | Particulars | J.F. | (₹) | Date | Particulars | J.F. | (₹) |

| 25.4.22 | To, Bal c/d | 10,00,000 | 25.4.22 | By, Bank of BB A/c | 2,50,000 | ||

| 25.4.22 | By, AA Pharmaceuticals A/c | 7,50,000 | |||||

| 10,00,000 | 10,00,000 | ||||||

| By Bal b/d | 10,00,000 |

Salary Account

| Date | Particulars | J.F. | (₹) | Date | Particulars | J.F. | (₹) |

| 30.4.22 | To, Salary Payable A/c | 15,000 | 30.4.22 | By, Bal c/d | 15,000 | ||

| 15,000 |

Salary Payable Account

| Date | Particulars | J.F. | (₹) | Date | Particulars | J.F. | (₹) |

| 30.4.22 | To, Bal c/d | 15,000 | 30.4.22 | By, Salary A/c | 15,000 | ||

| 15,000 | 15,000 | ||||||

| 1.5.22 | By Bal b/d |

Cash Book

Any organisation enters into numerous transactions during an accounting period, and amongst those a majority of the transactions get settled (either received or paid) involving cash. For this purpose, a separate book of account is maintained for recording only the cash transactions (whether effected in liquid cash, cheque or online transfers).

The book of account that records all cash receipts and cash payments of an organisation is referred to as cash book. The receipts are entered on the debit side, while the payments are recorded in the credit side of the cash book.

Features of Cash Book

Types of Cash Book

For the purpose of recording cash and bank related transactions at one place cash book is maintained. These cash books can be broadly classified into two categories – Regular Cash Book and Petty Cash Book.

1. Regular Cash Book: The cash book which records all cash and sometimes bank related transactions of an entity is called the Regular Cash Book or simply Cash Book. Such cash book can be classified into the following categories based on the number of amount columns maintained on each side of the cash book.

● Single Column Cash Book: In this cash book, only one amount column is maintained on each side to record transactions involving liquid cash. This type of cash book is usually maintained by the small organisations which do not have any bank account.Sometimes an organisation having a bank account can also maintain a single column cash book and open a separate bank account in the ledger. This cash book is actually the cash account of the entity.The balance of this cash book represent cash-in-hand at a particular point of time. The proforma of the single column cash book is a under:

Cash Book (Single Column)

| Date | Particulars | L.F. | Cash(₹) | Date | Particulars | L.F. | Cash(₹) |

● Double Column Cash Book: In many cases, two amount columns are maintained by organisation on each side of the cash book. This type of a cash book is called Double Column Cash Book. It is a popular practice to add an amount column to each side – the additional column to record the banking transactions entered into by an entity, instead of opening a separate bank account in the ledger.The balance of this cash book reflects the amounts of Cash-in-hand as-well-as Cash-at-bank at a particular point of time. The proforma of the double column cash book is a under

Cash Book (Double Column)

| Date | Particulars | L.F. | Cash(₹) | Bank(₹) | Date | Particulars | L.F. | Cash(₹) | Bank(₹) |

This type of cash book gives rise to a unique type of entry referred to as the Contra Entry. When any transaction takes place involving Bank A/c and Cash A/c, the posting will happen on both side of the same account (here, the Double Colum Cash Book). Examples of such transactions are: Deposit of cash into bank, Withdrawal of cash from bank etc. For recording such a transaction, the letter ‘C’ is written on both sides in the Ledger Folio (L.F.) column.

● Triple Column Cash Book: A Cash book with three amount columns on each side (namely Cash, Bank and Discount columns) is called the Triple Column Cash Book. The discount columns of each side represent separate discount accounts. Specifically, the discount column of the debit side of cash book represent Discount Allowed and that on the credit side represent Discount Received.

Conceptually, there are two types of discounts – Trade Discount and Cash Discount. The former discount is allowed by the seller to the buyer for making bulk purchases, while the later is allowed to encourage the buyer to make prompt payment. Trade discount is never recorded in the books of account. It is the Cash Discount which is recorded in the discount columns of the treble column cash book.

Further it is to be noted that unlike the cash and bank columns, the discount columns are not balanced; rather they are transferred to the respective discount accounts in general ledger. To be specific, the total of the debit side discount column represents the total discount allowed during a period and it is transferred to Discount Allowed Account in the general ledger, while the total of the credit side discount column represents the total discount received during a period and it is transferred to Discount Received Account in the general ledger. The proforma of the double column cash book is a under:

Cash Book (Trible column)

| Date | Particulars | L.F. | Cash(₹) | Bank(₹) | Discount(₹) | Date | Particulars | L.F. | Cash(₹) | Bank(₹) | Discount(₹) |

Multi-columnar Cash Book: This is a customized form of cash book that is maintained by organisations where huge cash transactions take place under certain fixed heads. Generally, organisations like clubs, schools, colleges etc. maintain this type of cash book. The proforma of the multi-columnar cash book is a under:

| Date | Particulars | Subscription | Duration | Intrest Received | Misc. Income | Date | Particulars | Salaries & Wages | Rent & Taxes | Communication Chrgs. | Misc. Expenses |

2. Petty Cash Book: In organisations where the number of cash transactions are numerous, it becomes tough for one personnel to handle and record all cash and bank related transactions. In such a case, the cash handling is split between two groups – one group handling petty cash transactions and the other handing transactions other than petty cash. This gives rise to a specific type of cash book called the Petty Cash Book. This book of account records only those cash transactions which are not of heavy amount, but the type of transactions are frequently entered into by an entity. The cashier in charge of the petty cash book is known as the Petty Cashier, the cashier of the other group is called the Principal Cashier or Chief Cashier.

The amount of petty cash is provided to the petty cashier either on Ordinary System or on Imprest System. Under the Ordinary System, a pre-decided amount of cash is given in lump sum by the chief cashier to the petty cashier. When the entire amount of petty cash gets spent, the petty cashier submits the details of petty expenditures to the chief cashier for review, and reimbursement.